With an increasing number of neo banks emerging and getting more news coverage, I thought it would be interesting to analyze the effect of FinTech companies on traditional banks. There are broadly three types of startups currently receiving a large amount of VC funding, looking to challenge traditional banks. The first kind are building robo advisors and other complimentary financial advisory tools to replace the good old (human) financial advisor. Then there are money transfer businesses such as TransferWise (now called Wise) eating into traditional banks’ high fees for such services. Finally, neo banks are digitally native, fully fledged banks that offer convenience and efficiency to their customers as well as zero maintenance fee accounts. With an anticipated wave of consolidation there will be increasing overlap within these categories over the coming years.

I believe the preference for investing in passively managed exchange-traded funds (“ETFs”) and mutual funds is a good predictor for what will happen within the wealth management industry. Ultimately, the more a firm automates its services, the less fees it needs to charge. Without having to pay fund managers, the profit margins are much larger for the entities that create ETFs and mutual funds. Actively managed ETFs and mutual funds were always attractive because they provided investors with broad diversification, professional management, and daily liquidity at a relatively low cost. Passively managed funds take the benefits of investing in broad diversified portfolios to the next level by minimizing fees further. They offer even lower operating costs, greater transparency, flexible trading, and often better tax advantages.

Similarly, new companies and apps automate financial planning and supply software to track budgets and investments. This makes classical financial advisors a more expensive and less convenient way for people to manage their money. Companies like BodesWell offer technological tools to help people with their financial decisions the same way financial advisors would.

While this inevitable transition occurs, there are also tools being created for the “modern advisor” to use. Startups are creating platforms to help traditional financial advisors handle more clients at once, and to better communicate with them. Addepar is a wealth management platform designed to aggregate all the clients’ ownable assets that helps to deliver comprehensive portfolio views and reporting to clients. Fewer advisors are also needed with the platform offered by ForwardLane, a data driven AI platform to generate financial insights, automating 80% of daily data analysis.

These innovations will cause large banks to trim down their wealth management groups and adjust their services. Even the tools created to increase the reach of current financial advisors will lead to a reduction of wealth management staff because there will be less manpower required. Traditional banks will likely fight back with their own robo advisors in an attempt to keep their current customers, and to continue acquiring new customers as these startups become increasingly popular.

The banking experience will be mostly digital within the next 10 years. This may result in poorer service for those who are part of the older generation and are not tech savvy. They will not necessarily trust themselves to manage their money without speaking to a (human) financial advisor. And as brick-and-mortar banks continue to close, it will be much more difficult for them to get service from an in-person advisor. However, traditional wealth management firms who focus their financial advising staff on high-net-worth individuals may have some leeway before the industry completely evolves, as they can still rely on human-to-human client interaction.

For so many years banks have been charging their customers high fees for every transfer or wire. Today, there are so many other enticing platforms that allow customers to transfer money for little or no cost. (Transfer)Wise facilitates international money transfers and exchanges for one third compared to traditional banks. Revolut makes managing foreign exchange easy and affordable. Venmo allows people to send friends and family money in a simple, quick, and free process. It is becoming a race to the bottom for the lowest fees between banks and neo banks. A key driver for this development may also be the rise of cryptocurrencies. Cryptocurrency technology provides people with the luxury of transferring money to anywhere in the world without any transaction fees at all. Now that this technology exists, why would anyone ever pay fees to transfer money again?

As neo banks are growing, they’re heavily disrupting the consumer banking market. They conveniently allow customers to access all their financial information from anywhere. A few examples are Chime, MoneyLion and Tala. Chime offers on the go banking services without minimum balance requirements, monthly fees, or foreign transaction fees. MoneyLion is a successful neo bank with products for borrowing, saving, investing, rewards, points, incentives and more, all at the tip of customers’ fingertips. Tala is a mobile application that makes the loan process easy and accessible for everyone. Brick-and-mortar banks are finding it difficult to compete with the convenience offered by these mobile first startups.

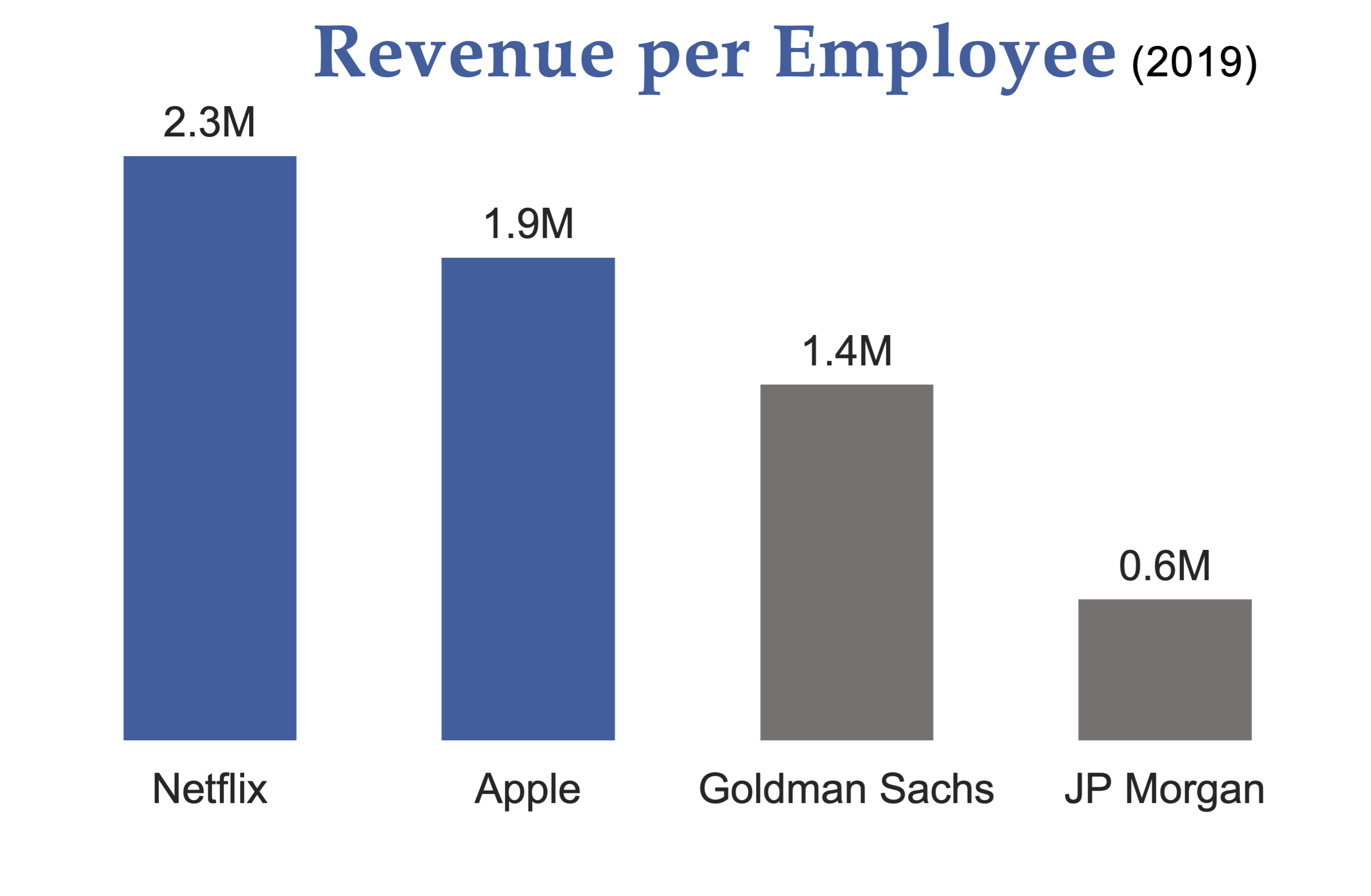

With VCs fueling these FinTech models, traditional banks are forced to adjust their services and cut down their staff to become more like tech companies. Many banks, like Goldman Sachs, have openly stated they are aiming to morph into tech companies. This means that they will have to cut their headcount dramatically in the process. Top tech companies generate much more revenue per employee. In 2019, Netflix’s revenue per employee was $2.3M and Apple’s was $1.9M; compared to Goldman Sachs which was $1.4M, and JP Morgan which was $554K (2019 happened to be one of these bank’s best years in terms of this ratio). Of course, as banks cut down their staff in certain areas, there will still be labor-intensive parts of the banks like investment banking. Most retail banks today also offer mobile apps for their customers to view their account information, deposit checks and manage their account in other ways but banks will need to gain the operational efficiency of a tech company to successfully compete in a no/low fee world.

It will be interesting to see how this ultimately plays out. The current banking landscape in the U.S. is a few large conglomerates, and a long tail of smaller local/ community banks. These local banks have survived because people like the convenience of taking care of their banking in their neighborhood at a brick-and-mortar shop. How will the market map look as more neo banks emerge? Will neo banks replicate this model? These questions are crucial for a VC investor with a focus on fintech. The outcome will determine how much room there is for competition within this space.

It is possible that as the banking market turns digital, there will be no need for these smaller banks. Once people take care of all their banking needs online, why would they need a local bank? It is likely that unlike the current banking landscape, the entire market will consist of a few conglomerate neo banks. On the other hand, maybe smaller neo banks will target online communities as opposed to geographic communities. They could try to narrow down their target market by appealing to specific groups of people with different interests or agendas. A neo bank with a certain culture could attract people if the banks values align with their own. Additionally, neo banks can offer benefits for students at universities or employees of businesses.

Large conglomerate banks may ultimately be in a good position to leverage these technological innovations themselves or acquire digital newcomers. While traditionally slow to change, they have the necessary capital and resources to innovate and make acquisitions. They can shrink their workforce and invest in R&D to build technology that can compete with neo-banks or integrate them. Smaller community banks, however, may not be as fortunate as the banking world turns digital.