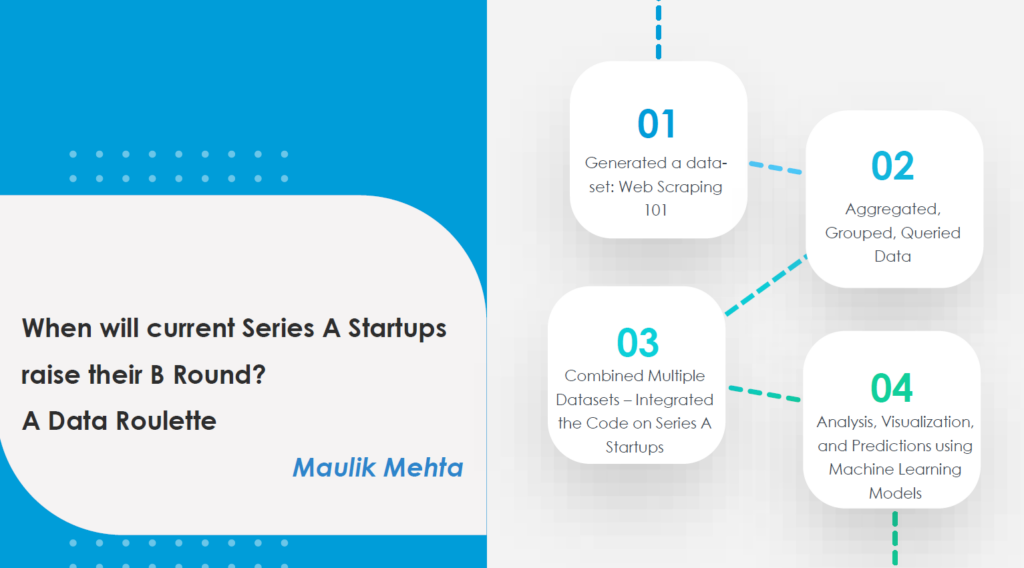

Someone recently asked me this question, so I built a prediction model to help generate an answer. Keep reading as I discuss my process and give actual Series B predictions.

Where to begin?

I began by pulling together metrics that made sense for a company trying to raise a Series B. My thinking first went to a company’s finances and whether they seem attractive to venture investors.

- The company should achieve $10M in Annual Recurring Revenue (ARR).

- The startup should grow 50% over the last two years with a 70% gross margin and 90% retention.

- The company should have a diversified customer base and a strong LTV/CAC Ratio (Lifetime Value / Customer Acquisition Cost).

The issue here is that we are talking about private companies, and their financial information is not readily available. So, I started speaking about this more and more with my team and other fund managers. These discussions presented more data points that we look at:

- The amount of cash raised in the last financing round and total?

- What is the current burn rate?

- How many founder shares have been diluted?

In reality, it is difficult to predict when a company would or could raise their Series B financing round, even if all of these variables are known. This problem motivated me to create a prediction model using data science and machine learning techniques.

Building the dataset

To build a predictive model using machine learning, you need to start with a dataset. I began scraping and extracting web content of over 700+ companies that raised a Series A and/or a Series B round in the last six years. Once this was generated, I cleaned the data by removing redundant variables, and also created new variables like the following:

- Year Founded

- Length of time between Year Founded and Series A

- Difference between Series A and Series B pre-money valuations

- Length of time between Series A and Series B

(Actually, there were a lot more variables 😊 – appropriately showcased in Figure 1)

I used these inputs in a random forest regression analysis. The table below is a sample representation of how I trained the model. There are five companies below in Table 1 that have all raised a Series A and Series B rounds within the last six years. This makes it easy compare differences in employee count, pre-money valuation, and time between the Series A and Series B rounds.

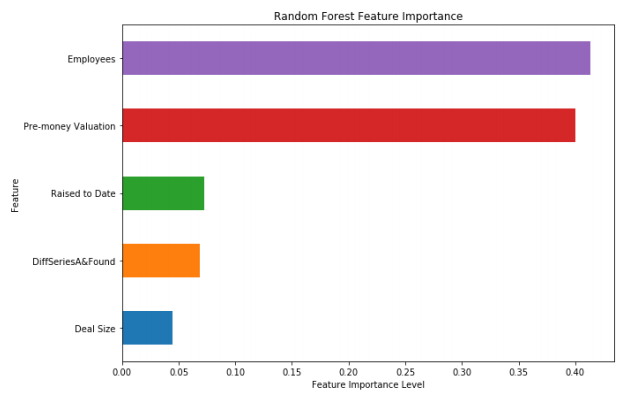

In looking at the random forest regression’s feature importance weighted scores, the following filters were given the highest weight for predicting an upcoming Series B Round.

- Difference in numbers of employees from Series A to Series B

- Difference in mark up in Pre Money-Valuation from A to B

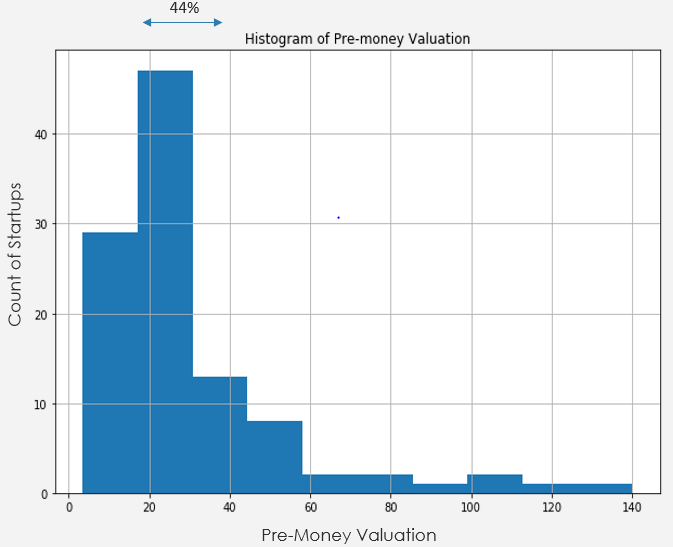

The new addition of capital is directly linked to an incredible markup in the employee count. A startup would receive a ton of inbound interest after publishing that they have raised a new round. See the histogram below for a complete list of weighted scores.

Additional insights from the data:

The three main data points I found interesting are:

- Within 3 Years of being founded, 83% of startups raise their Series A, and 66% of these startups go on to raise a Series B.

- Series A startups take 10-18 months before raising their Series B financing round.

- A little less than half of Series A startups (44% to be precise) have a pre-money valuation of $20M-$30m before raising their Series B Financing round.

So, who is likely to raise?

This is the real reason why you kept reading. After running the prediction model – below is the group of Series A companies that could end up raising their series B Round in the next four quarters starting in Q2 2021.

It would be fair to assume that the model does not take into consideration financing rounds that are pre-empted or companies coming out of stealth raising large Series A rounds. Startups closed out 2020 in a much stronger position than the one they started the year in, with global venture funding up 4 percent year over year to $300 billion. Moreover, deal volume has grown significantly through the decade. For Instance, 2011 featured 10,000 rounds from seed to late-stage mega-rounds, and now, the deal volume is close to 30,000 rounds (seed to late-stage) since 2017.

However, after looking at the results and the histograms above, the model could do well.

*As I was writing this blog post, a Techcrunch article came out announcing that Privacy rebranded to Lithic and raised a $43M Series B round. According to my prediction, I was off by a quarter.

Good luck investing!

I hope you enjoyed reading. I would love to continue the conversation if you want to play around with the model or if you are one of the companies mentioned in the prediction analysis, and I got it wrong.

To learn more about me and what is going on at Arc Ventures follow us both on Twitter: @MMaulik11 and @Arc_Ventures. Shoutout to Rachel Payne and Eric Kohlmann for helping me structure the blog post.